If the thought of preparing your 1120S tax return stresses you out, you are not alone. Many S-corporation owners feel confused by Schedule K-1 allocations, unsure about shareholder basis, or worried that a mistake could trigger an IRS audit. Often, owners just receive a completed return to sign without understanding how the numbers affect their personal liability.

This guide is different. It breaks the process into clear, step-by-step instructions. You will move from simply signing forms to understanding your return and making smart decisions. This approach helps you optimize your tax results and keep your company’s finances healthy.

For extra support, our team at Acct. Right, PLLC offers professional business tax preparation services. We help turn this yearly task into a strategic advantage for your business

IRS Form 1120S: What S Corporation Must Know

Form 1120S, officially the U.S. Income Tax Return for an S Corporation, is essential for businesses that have elected pass-through taxation. Unlike C corporations, which file Form 1120, S corps report income, losses, deductions, and credits that flow directly to shareholders’ personal returns, avoiding double taxation, and are reported on their individual tax returns through Schedule K-1

According to the IRS, S corporations must file Form 1120-S by March 15 each year, which is two months and 15 days after the end of their tax year.

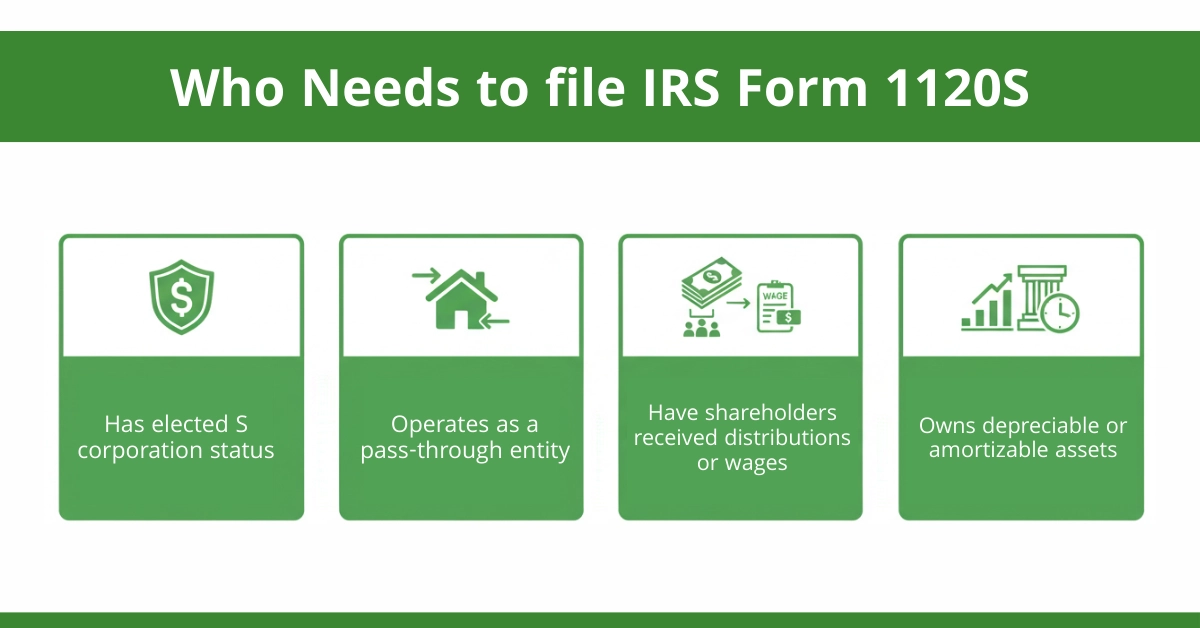

Who Needs to file IRS Form 1120S

You must file if your business:

- Has elected S corporation status

- Operates as a pass-through entity

- Have shareholders received distributions or wages

- Owns depreciable or amortizable assets

This applies across industries, including healthcare providers, real estate professionals, and growing businesses with multiple owners.

Key Difference between 1120 vs. 1120S

| Feature | Form 1120 | Form 1120-S |

| Taxation | Entity-level tax | Pass-through |

| Shareholder reporting | Dividends | Schedule K-1 |

| IRS scrutiny | High | Higher if misallocated |

Errors in S corporation filings often create personal tax issues for shareholders, which is why accuracy matters.

Common Points in 1120S Preparation:

Most challenges business owners face fall into a few key areas:

Schedule K-1 & Basis Confusion: Shareholders must track their “basis,” which represents their investment in the company. If the basis is incorrect, losses may be disallowed, or distributions may become taxable unexpectedly.

Reasonable Compensation issues: The IRS requires shareholders-employees to receive a “reasonable salary” before tracking non-wage distributions. Setting this too low is a common audit trigger and can lead to payroll tax penalties.

Bookkeeping Disconnect: Financial records not being “tax-ready” at year-end causes delays and errors.

Missed Deductions & Credits: Without deep tax knowledge, owners may overlook industry-specific write-offs, such as certain equipment deductions and R&D credits that can be particularly relevant in technical or service-based fields

Preparing an accurate 1120S tax return requires a clear understanding of pass-through income and available deductions. One key component often prepared alongside Form 1120S is the Qualified Business Income deduction, explained in detail in Form 8995. Reviewing this guide helps ensure compliant and optimized S-corporation tax filings

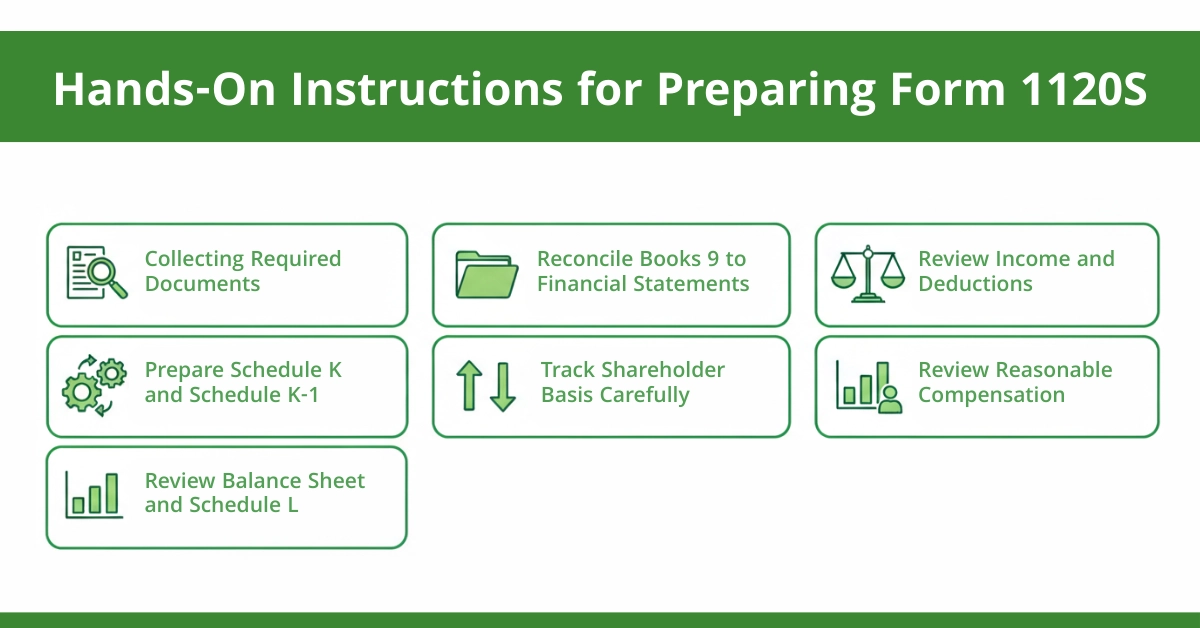

Hands-On Instructions for Preparing Form 1120S

Step 1: Collecting Required Documents:

Before starting Form 1120-S, collect:

- Profit and Loss statement

- Balance Sheet

- Payroll reports (W-2s, W-3, Forms 941)

- Prior-year tax returns

- Shareholder loan and capital records

- Bank and credit card statements

Healthcare practices should also gather RCM billing reports showing charges, collections, adjustments, and write-offs.

Step 2: Reconcile Books 9 to Financial Statements

- Match bank balances to accounting records

- Separate personal and business expenses

- Confirm payroll totals match filed reports

Clean books reduce errors and prevent amended returns.

Step 3: Review Income and Deductions

Start with gross receipts, subtract returns and allowances, then apply allowable deductions. For healthcare providers, this means aligning

RCM system reports with actual deposits, accounting for timing differences between cash and accrual methods.

Step 4: Prepare Schedule K and Schedule K-1

- Allocate income and deductions based on ownership percentages

- Adjust for shareholders who joined or left mid-year

- Ensure Schedule K totals match all K-1s exactly

Mistakes here directly affect shareholder personal tax returns.

Step 5: Track Shareholder Basis Carefully

- Begin with prior-year basis

- Add income and capital contributions

- Subtract losses and distributions

- Document ending balances

This step is often skipped by competitors but is critical for tax accuracy.

Step 6: Review Reasonable Compensation

Confirm:

- Owners received wages through payroll

- Payroll taxes were properly withheld and paid

- Distributions are clearly separated from wages

Improper compensation is one of the IRS’s most common audit triggers.

Step 7: Review Balance Sheet and Schedule L

- Assets must equal liabilities plus equity

- Loan balances should match documentation

- Retained earnings and AAA accounts must be accurate

Balance sheet inconsistencies increase audit risk.

Common Errors to Avoid

Missing or incomplete documentation tops the list of preparation mistakes. Without proper records, you’ll struggle to make sustainable deductions during an audit. Keep organized files throughout the year. Incorrect shareholders’ allocation creates significant problems. All items must be allocated based on ownership percentages and stock ownership periods. Mid-year ownership changes require daily proration calculations.

Tax Deductions and Credits for S Corporations

Business Expenses in Healthcare Settings

Medical practices can deduct ordinary and necessary expenses, including:

- Medical supplies and equipment

- Professional liability insurance

- Continuing medical education (CME)

- Healthcare RCM tax strategy consulting fees

Remember: expenses must be substantiated. The IRS publication 535 provides clear guidance, but many practitioners miss the requirement to allocate personal vs. business use.

Depreciation and Amortization Impact

Section 179 deduction allows immediate expensing of qualifying equipment up to $1,160,000 (2024 limit). For S corporations with multiple shareholders, this deduction flows through and may be limited at the individual level by business income thresholds.

Impact on RCM Revenue

Revenue cycle management complexities create unique deductions. Bad debts written off after collection efforts fail, contractual allowances from insurance payers, and merchant fees from patient payment platforms all reduce taxable income. Track these in your financial modeling to project quarterly estimated taxes accurately.

Filing and Submission Process

Electronic Filing vs. Paper Filing

The IRS mandates e-filing for corporations filing 250+ returns annually, but we recommend electronic submission for all clients. Benefits include:

- Immediate confirmation of receipt

- Faster processing (typically 3 weeks vs. 6-8 weeks)

- Reduced error rates (system validations catch common mistakes)

Deadlines and Extensions

The March 15 deadline looms large for S-corps. File Form 7004 by this date to receive an automatic 6-month extension. Critical point: an extension extends the filing deadline, not payment. You must estimate and pay tax due by March 15 to avoid penalties.

Why Hands-On Preparation Matters

Hands-on preparation helps owners:

- Understand where numbers come from.

- Spot issues before tax season.

- Make informed compensation and distribution decisions.

When combined with professional oversight, this approach leads to better compliance and smarter tax planning.

Tips for Healthcare Practices & RCM Professionals

Aligning Tax and Billing Records

Your healthcare RCM tax strategy must reconcile daily. Monthly, compare:

- RCM software revenue reports to bank deposits.

- Adjusted collections to gross charges.

- Write-offs to bad debt expense.

This alignment catches issues like unrecorded insurance recoupments that could inflate taxable income.

Avoiding Compliance Issues

Healthcare S-Corps face unique compliance requirements:

- Stark Law and Anti-Kickback implications for physician distributions.

- Proper reporting of provider bonus structures.

- Documentation for equipment purchases exceeding $2,500 (requiring capitalization).

Conclusion:

Preparing 1120S tax return hands-on transforms compliance from a feared chore into a strategic advantage. You’ve learned the critical steps: document collection, Schedule K-1 accuracy, basis tracking, and healthcare-specific considerations. More importantly, you gain clarity on the purpose behind each step.

At Acct. Right, PLLC, we don’t just prepare returns, we build your financial literacy. Whether you need Business Tax Preparation (1120, 1120S, and 1065), Fractional CFO Services for ongoing guidance, or Financial Modeling to project next year’s tax impact, our Dallas-based team serves clients nationwide.

Disclaimer:

This material is provided for general information only and should not be relied on as legal or tax advice. Tax rules change and vary by situation. Professional guidance is recommended. Some images may be illustrative or AI-generated.

Frequently Asked Questions

What raises red flags with the IRS for S corporations?

Low owner wages, mismatched K-1 allocations, unbalanced Schedule L, and inconsistent revenue reporting commonly trigger S corporation IRS scrutiny reviews.

What is the $2,500 expense rule?

The $2,500 de minimis safe harbor allows expensing smaller asset purchases instead of capitalizing, if accounting policy exists and elections.

What is the 5-year rule for S corporations?

The five-year rule limits re-electing S status after termination, preventing frequent switching between C and S tax treatments for corporations.

What is the 2% rule for S Corp?

Shareholders owning two percent or more must include certain fringe benefits as taxable wages, unlike regular employees for S corporations.

Does the IRS always catch mistakes?

The IRS does not catch every error, but automated matching and audits often identify inconsistencies years later during reviews cycles.